I really didn’t want to do IVF, but it seemed like it was our only option now.

I’d been worried about the prospect of IVF being our only choice ever since our first doctor’s appointment at the clinic. It’s expensive and invasive, and I did not want to go down that road.

Read more: What Do You Mean It’s Not Covered?I was mostly worried about the cost. But I learned the Colorado legislature passed a bill (HB20-1158) requiring insurance providers to cover the cost of infertility treatments, including IVF. Governor Polis signed it into law in April 2020, and it would take effect in January 2022.

OK. Maybe we can do this. We set aside some funds when we sold our old house. I’d also set aside the max amount in two years’ worth of Flexible Spending Accounts (FSA). Maybe we could afford it after all.

Open enrollment comes around for both my employer and Nick’s, and we did our best to figure out if they’d be covering the procedure. No luck with my employer, but the benefits company my husband’s employer used looked like they did.

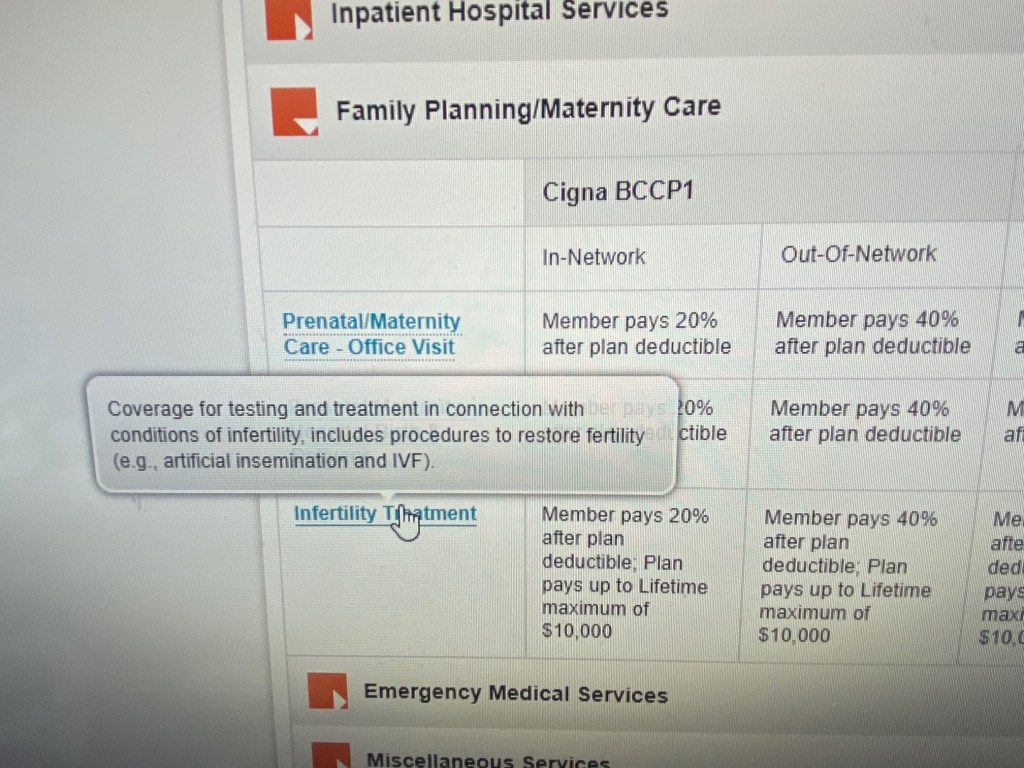

When listing examples of their coverage, under infertility, IVF was listed as an example of a covered procedure. With the insurance we chose, it would be 50% coverage. (We got this info from the screenshot at the top.)

That’s a heckuva lot better than nothing when dealing with something as expensive as IVF.

With the money we’d set aside and my FSAs, we should have enough to cover our half plus the medications I’d need. This was starting to feel doable.

I still wanted to confirm it, over the phone, to be absolutely sure, so we called his benefits company to ensure it was a covered procedure. The customer service rep discussed it with her supervisor and then confirmed it was.

We decided to switch to Nick’s insurance, even though they have a “spousal surcharge” to dissuade spouses who have access to their own insurance from getting on his company’s insurance. (Seems awfully skeezy to me…)

Though we hated to pay that extra charge when my employer doesn’t do that, we knew it’d save us money in the long run since IVF was covered.

Fast forward to when we’re sent our first financial agreement from the fertility clinic in April 2022. Total due: $17,875. I wrote back – I don’t think that’s correct. We were told our insurance covers it at 50%.

The financial counselor tried running our insurance again: Sorry, it doesn’t look like it’s covered.

This began a weeks’ long effort to get to the bottom of the situation with both our insurance company and the benefits provider.

We were told wrong.

A very summed up and paraphrased version of those conversations looks like this:

_________

Benefits Co. (BC): The rep who told you that shouldn’t have told you that.

Me: OK, well how are you going to make this right? Are you going to pay the half that you said was covered?

BC: IVF was only listed as an example, it doesn’t mean it’s covered.

Me: Do you understand how incredibly misleading that is? Let’s say I needed a kidney transplant, and I saw that “organ transplants (e.g. kidney, liver, heart, lung, etc.)” was listed on your website as covered procedures. And then you tell me kidneys aren’t covered. That doesn’t make sense. That’s also not how the English language is used…

BC: Well, it’s not covered, and we’re not paying for the half we told you was covered.

Me: Can you at least remove the spousal surcharge? We never would’ve chosen to enroll in this insurance had we been correctly told IVF wasn’t covered. I have the same coverage available through my work without the surcharge.

BC: We’ll talk with the company and get back with you.

A week or so later…

BC: We cannot remove the spousal surcharge. The only way to do it is to remove you from your husband’s plan.

_________

This was absolutely maddening. A company used incredibly misleading verbiage to describe their coverage and then a rep told us a procedure was covered when it wasn’t.

And there’s nothing we could do about it. Sure there may have been some legal options, but none of them would be worth any lawyer’s time. We’re talking about $9k, maybe $10k, in damages. That’s it. Not worth litigating over.

After that, it felt like we were back to square one. We’d had enough money to cover our half and medications, but not the whole bill. Sure there are lenders out there who focus on fertility lending, but we’re trying really hard to pay off debt – not go into more of it.

To me, the difference between 50% coverage or no coverage is having a family vs. not having a family. Pretty big deal.

Fortunately, my parents came to the rescue. They offered to help us cover the amount we didn’t have so we could go ahead and start the process.

“Anything to get some baby Jacksons,” they said.

I am beyond lucky to have the parents I do.

One response to “What Do You Mean It’s Not Covered?”

[…] our IVF cycle was going to be covered by insurance. Finding out it wasn’t was a shock, and fighting with the insurance provider added another layer of […]

LikeLike